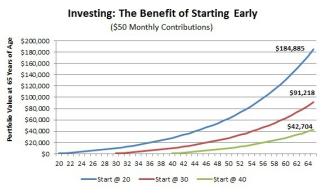

The magic of compounding means anyone who starts saving at a young age, say in his or her early 20s, and lives until old age, can build wealth by saving relatively little each year compared to someone who starts much later. If you’re a young person who has established an emergency fund, owes little-to-no debt, and can easily afford your monthly living expenses, you may be ready to begin a lifelong investing journey!

Here are the first three accounts we typically point young investors to as they gain experience and accumulate assets and income:

1.Maximize contributions (up to $19,500 in 2021) to your employer’s 401(k) program and capture the full employer match if possible. If offered, a 401(k) defined contribution retirement plan with an employer match offers “free money” by doubling, in some cases, your contribution up to a certain percentage. Money can be saved either pre-tax, directly from your paycheck, or post-tax, in a Roth 401(k), provided your income level qualifies.

2.Open and fund a Roth IRA (up to $6,000 in 2021). These post-tax accounts allow contributions to grow tax-free, and withdrawals can be made tax-free in retirement with no required minimum distributions. Furthermore, you can withdraw contributions tax-free at any time, for any reason, making this a more liquid form of retirement savings than a 401(k) account (early withdrawal of earnings, however, will incur a 10% penalty fee).

3.Open and fund a taxable investment account. This is an account where you can actively invest in the market and move money in and out of the account easily. Low and no-fee funds, like ETFs and index funds, following a diverse asset allocation strategy are often attractive investment vehicles for younger investors new to the discipline.

SOURCE: New York Times

Learning to be a successful investor is a gradual process and the investment journey is typically a long one. When you are young, you can take more risks in the market because you have time for the market to recover, but as you get older, you will need to be more conservative in your investments. A Cranbrook Wealth investment professional can help you with this transition and guide you toward balanced portfolio that reflects your investment budget and goals as you gain experience.